By Ole Hansen, Head of Commodity Strategy at Saxo Bank

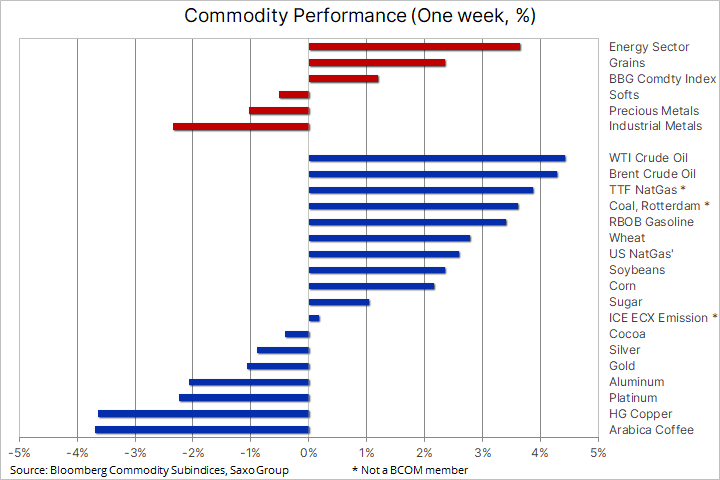

Commodities traded mixed during the first week of June with buying fatigue emerging in both precious and industrial metals, while grains and especially the energy sector rose. Overall, the Bloomberg Commodity Spot Index reached a fresh ten-year high despite worries that stronger-than-expected macro data from an overstimulated U.S. economy could see the Federal Reserve start talking more openly about reducing support.

Rising inflation concerns, increased demand for green transformation metals, OPEC+ keeping a stranglehold on supply, and weather concerns are all likely to continue fueling a broad rally during the coming months. In the very short-term, however, several commodities have seen loss of momentum while others have become overbought, thereby raising the risk of a swift correction including most of the metals and coffee.

Crude oil broke higher ahead of the latest OPEC+ meeting where the group, as expected, decided to stick to its planned July increase, but in weighing up the prospect for a continued recovery in demand and uncertainties about an Iran nuclear deal, the group refused to give any hints about their next move. While the recovery in global fuel demand remains far from synchronized due to concerns over tighter Covid-19 related restrictions in Asia, the market seems happy in the short-term to focus primarily on the positive demand outlook in the U.S. and parts of Europe.

These developments have nevertheless helped tighten market conditions with OPEC forecasting an undersupplied global market into the second half, of course barring any additional barrels from OPEC+, Iran or U.S. shale. The recent run up in prices which culminated in Brent challenging a key area of resistance around $72 and WTI reaching a 2018 high has been led by WTI crude oil amid seasonal-low U.S. gasoline stocks ahead of an expected busy summer driving season and crude stocks at Cushing, the WTI delivery hub, trailing the five-year average. This has been compounded by no clear signs yet of rising production from the former boom and bust shale oil sector, which has now turned much more disciplined in its approach to rising oil prices.

Source: Saxo Group

Gold was set for its worst weekly decline since March after it finally succumbed to a bout of profit taking following the strong run-up since early April. During this time, and especially during the past month since breaking above key technical levels, an underlying bid from long-term trend-following funds had kept the market on a steady rise. But after having traded in overbought territory for the past two weeks, the risk of a correction had grown and once the remaining buy orders from the FOMO traders (fear of missing out) had been filled, it took one strong U.S. data point to send it sharply lower.

Pressured by a stronger dollar and rising yields following a raft of recent strong U.S. economic data, the market is once more focusing on the risk that the Federal Reserve may consider tightening the market earlier than previously thought. Gold managed to claw back some of the earlier losses following Friday’s softer than expected U.S. non-farm report.

From a technical perspective, the loss of momentum below the 21-day moving average highlights the risk of additional short-term weakness towards the 200-day moving average, currently at $1841. If gold manages to bounce before reaching that level, let alone $1825, the 38.2% retracement of the recent rally, this latest setback will be viewed as a small correction within a strong uptrend.

Source: Saxo Group

Copper ended up near the bottom of the weekly performance table, probably the first time this has happened since the commodity rally gathered steam some nine months ago. The recent loss of momentum had raised the risk of a deeper correction from financial investors focusing more on short-term technical price developments than the long-term prospect which still points to higher prices with the possibility of inelastic supply struggling to meet an expected pickup in demand, not least as the electrification gathers pace.

In addition to this, some weakness in Chinese demand has emerged with the key Yangshen copper premium of the LME falling to a four-year low, while in London the spread between spot copper and the three-month contract has traded in contango (oversupply) for the past three weeks. Furthermore, stocks at exchange-monitored warehouses stocks have stabilized near a ten-month high while speculators have cut their net-longs by 63% since December.

However, while the short-term risk appetite may have diminished, the positive story has not suddenly gone away, and we suspect buyers will return sooner than expected to prevent the price making a return to the trendline from early October, currently at $4.18. Before then, additional support can be found in a five cents band between $4.38 and $4.43 as per the chart.

Source: Saxo Group

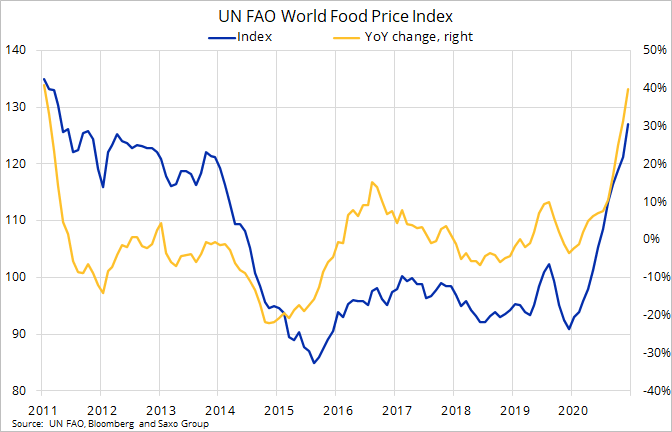

Agriculture: Global food costs surged to a fresh decade high in May, according to the UN FAO’s Global Food Price index which rose 4.8% to record a year-on-year increase of almost 40%. The index covering 95 price quotes showed a rising trend in all five food groups led by sugar, oils and meat. Drought in South America, record purchases by China and soaring demand for biofuel has left the agriculture market ill prepared for any additional production shock, hence the current intense focus on weather conditions in key growing regions across the Northern Hemisphere.

The pain of these increases will, just like a decade ago, hurt some of the poorest import-dependent nations at a time where most are still grappling with the economic fallout of the pandemic. One positive note, however, is that while agriculture commodities have surged higher, wheat and especially rice, two of the world’s most important food staples, have remained relatively subdued. High Protein Paris Milling Wheat trades 26% above its five-year average while Thai white rice, the Asian benchmark, only trades higher by 12%. The latter benefitting from the fact it is mostly produced for human consumption whereas others also see demand from livestock feed and biofuel production.